Under the Corporations Act 2001, financial product advice is classified as either “general advice” and “personal advice”.1 Personal advice is financial product advice that is given or directed to a person (including by electronic means) in circumstances where:

- The provider of the advice has considered one or more of the person’s objectives, financial situation and needs (otherwise than for the purposes of compliance with the Anti-Money Laundering and Counter-Terrorism Financing Act 2006 or with regulations, or AML/CTF Rules, under that Act); or

- A reasonable person might expect the provider to have considered one or more of those matters.

General advice is defined as financial product advice that is not personal advice.

The distinction between the two types of advice has caused much confusion for the financial planning industry since the implementation of the Future of Financial Advice (FOFA) reforms in July 2013. Unfortunately, despite the publication of ASIC’s Regulatory Guide 36 (“Licensing: Financial product advice and dealing”) and Regulatory Guide 244 (“Giving information, general advice and scaled advice”), there is still a need for judicial clarification.

There are far reaching implications for all financial planning businesses, as the provision of general advice does not require, inter alia, the issuing of a Statement of Advice (SoA) nor compliance with the Best Interests Duty (BID) obligations, as is the case with personal advice.

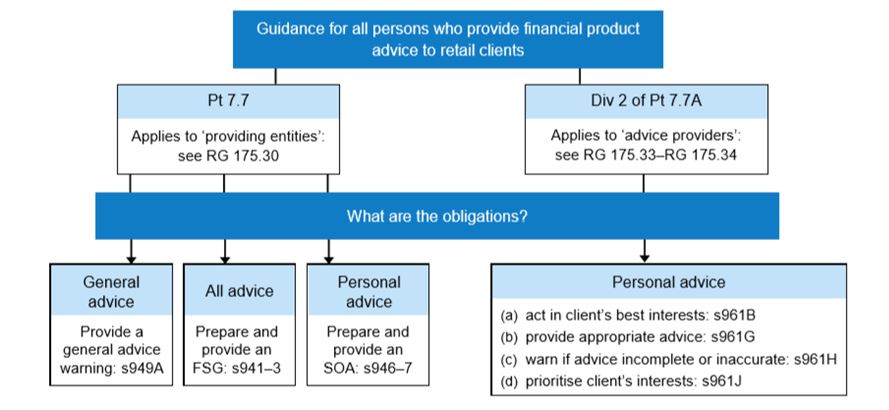

The following chart from RG 244 highlights the different obligations associated with the provision of general and personal advice. From an administrative / workflow perspective, it is clear that the provision of personal advice requires greater resources and expertise.

A providing entity is either an AFS licensee or an authorised representative.

An advice provider is generally the person who actually gives the personal advice and is either an AFS licensee, an authorised representative or other representatives of an AFS licensee. Where advice is provided through a computer program, the legal obligations apply to the legal person that provided the advice.

Advisers who intend to give only general advice may inadvertently be in breach of the licensing provisions of the Corporations Act if their advice was later found to be personal advice. This type of breach can occur if the AFSL only permits the provision of general advice. The following case will hopefully provide some much needed clarity.

ASIC v Westpac Banking Corporation

In late 2016, ASIC commenced legal proceedings against Westpac Banking Corporation (Westpac) over alleged breaches of the BID obligations. By way of background, Westpac was alleged to have established a call centre team and offered staff bonuses to convince clients to switch (rollover) $646.7 million in external superannuation savings into the bank’s own products.

A key issue to be determined is whether Westpac staff provided general or personal advice in their endeavours to persuade clients to switch their super to Westpac’s products. More specifically, the circumstances in which an advice provider would be assessed as having “considered” one or more of their client’s objectives, financial situation and needs would need to be determined.

It should be noted here that the guidance provided by RG 244 is limited, particularly as the mere possession of a client’s personal information does not necessarily mean that any advice provided would be personal advice (RG 244.46). Interestingly, however, at an Financial Ombudsman Service forum it was observed that the provision of insurance quotes (which would take into consideration a client’s personal details such as their age and nature of occupation) may be considered personal advice.

It may be that the presentation of several product choices to a client – even if an adviser does not make a specific recommendation – could be regarded as giving personal advice. This may be contrasted with newspaper “Q & A” columns in which financial experts purport to give general advice despite clearly having considered the personal situations of those submitting their questions. Unfortunately, until case law becomes available (the Westpac case is expected to run for some months), financial planning businesses must continue to operate with the somewhat confusing guidance from ASIC’s publications.

What should Financial Planning businesses do in the meantime?

Where it is unclear whether an adviser has provided “general” or “personal” advice, the conservative approach would be to comply with the obligations as applicable to personal advice, although this is inefficient and costly.

In addition, those who are only authorised to provide general advice based on their AFSL conditions, or authorisations from an AFSL holder, should exercise extra caution during the advice process.

Financial planning businesses would benefit from having Adviser Compliance Audits conducted on their advisers because this will be one way of mitigating regulatory risk.

Know Compliance is able to assist financial planning firms and other licensees to conduct Adviser Compliance Audits and also compliance audits of the financial planning firms and licensees. Contact us on +61 3 9689 1186.

1 Corporations Act 2001 (Cth) s 766B